Wills After Marriage: The Complete NRI Guide to Protecting Everything You Are Building Together

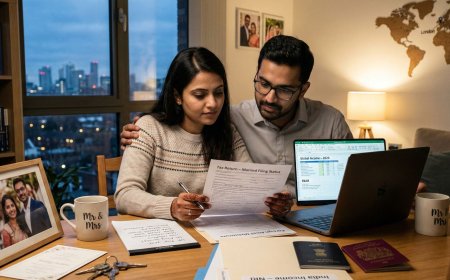

For newly married NRI couples with assets spanning multiple countries, a will is not an optional extra — it is one of the most important legal documents you will ever create. This complete guide covers everything NRI couples need to know about wills after marriage: what happens without a will under intestacy laws in India, the UK, USA, Canada, Australia, and UAE, the multi-jurisdictional will approach for NRI estates, the critical role of beneficiary designations on pensions and retirement accounts, specific provisions NRI couples should include, and the common mistakes that leave families in unnecessarily difficult situations. The most thorough will and estate planning guide written specifically for newly married NRI couples worldwide.

The Document That Protects Everything You Are Building

You have just done something remarkable.

You have built a life across borders — a career in an international city, assets in multiple countries, family connections spanning continents, a financial foundation that reflects years of deliberate effort and careful decision-making. You have found a partner who understands that life and who is building alongside you. You have celebrated that partnership with a wedding that brought two families and two cultures into the same space.

And now you are going home. The wedding week is over. The planning infrastructure that consumed eighteen months of your life has been dismantled. The vendors have been paid, the venue has hosted other events, the photographs are being edited. You are, finally, simply married.

In the weeks and months that follow, you will update your passport. You will change your name. You will add your spouse to your health insurance. You will review your joint budget. You will have the first of many conversations about your shared financial future.

And somewhere in that list of post-wedding administrative tasks, there is one item that most newly married NRI couples never get to. Not because they have decided against it. Not because they have considered it and found it unnecessary. Simply because it does not have a deadline, does not trigger a qualifying event window, does not produce an immediate consequence if it is deferred.

A will.

The conversation about what happens to everything you have built if one of you — or both of you — dies.

This conversation is uncomfortable. It involves contemplating outcomes that feel remote and incompatible with the optimism of a new marriage. It requires talking about death in a cultural context — the Indian family context, specifically — where such conversations are sometimes considered inauspicious, where talking about what happens after you die can feel like inviting the outcome.

And yet it is one of the most important legal documents a newly married NRI couple can create. Because without a will, the assets you have worked to build do not necessarily go where you would want them to go. Without a will, the legal framework that determines what happens to your estate is the one provided by default — by the intestacy laws of whatever jurisdiction happens to apply — rather than the one you would have chosen. Without a will, the person who must navigate the aftermath of your death — your spouse, your family — is left to do so without the guidance and clarity that a will provides.

For NRI couples whose assets span multiple countries, whose family relationships span generations and continents, and whose legal situation involves the intersection of multiple jurisdictions' laws — the will is not an optional extra. It is a necessity.

This article is the complete guide to will and testament considerations for newly married NRI couples. It covers why wills matter more for NRI couples than most, what happens without a will under the intestacy laws of each relevant country, the specific considerations for multi-jurisdictional estate planning, the practical steps for creating a will that works across jurisdictions, and the common mistakes that leave NRI families in unnecessarily difficult situations.

The Core Reality: Why Wills Matter More for NRI Couples

The case for creating a will is strong for any adult with assets. For newly married NRI couples, the case is considerably stronger — for reasons that are specific to the multi-jurisdictional, multi-asset, multi-family-obligation nature of NRI lives.

You Hold Assets in Multiple Countries

A typical NRI professional holds assets in at least two countries — property, bank accounts, pension funds, investment portfolios, and business interests spread across the country of residence and India, and potentially across additional countries where earlier career stages were spent.

Each country has its own laws governing what happens to assets located within its borders when the owner dies. Without a will that specifically addresses assets in each jurisdiction, the estate administration process requires navigating multiple legal systems simultaneously — with the intestacy laws of each jurisdiction determining how each set of assets is distributed.

This multi-jurisdictional administration, in the absence of a will, is substantially more complex, more expensive, and more time-consuming than the administration of a well-drafted estate plan. It is also less likely to produce the outcome the deceased would have chosen.

Indian Succession Law Is Not What You Might Assume

For NRI couples with Indian assets — property, bank accounts, investments — the Indian succession framework determines what happens to those assets in the absence of a will. And the Indian succession framework is not a single system. It is a collection of personal laws that apply differently depending on the religion of the deceased.

Hindu succession — governed by the Hindu Succession Act, 1956 — applies to Hindus, Buddhists, Jains, and Sikhs. Muslim succession is governed by Muslim personal law, which has its own structure of inheritance. Christian and Parsi succession is governed by the Indian Succession Act, 1925 — a more codified framework.

The Hindu Succession Act creates a class of heirs — Class I heirs including the spouse, children, and mother — who share the estate in defined proportions. This distribution may not reflect the preferences of the deceased. It may produce an outcome where assets are divided in ways that are practically inconvenient — property held in multiple shares by multiple family members, with attendant complications for management and eventual sale.

A will that specifically addresses Indian assets and directs their distribution according to the deceased's wishes prevents this default distribution and the complications it produces.

The Surviving Spouse May Not Be the Automatic Beneficiary You Assume

This is the insight that most surprises newly married NRI couples: in many jurisdictions — and particularly in India — getting married does not make your spouse the automatic primary beneficiary of your estate. The default distribution under intestacy rules often divides the estate among multiple heirs — including the spouse, children, and in some cases parents — rather than directing everything to the surviving spouse.

For a newly married couple without children, the intestacy rules may direct a portion of the estate to the deceased's parents rather than entirely to the surviving spouse. This may or may not reflect the deceased's wishes — but without a will, the deceased has no say in the matter.

Your Pension and Life Insurance Beneficiary Designations Also Need Updating

Separate from the will — and not controlled by the will — are the beneficiary designations on pension funds, life insurance policies, and retirement accounts. These assets pass directly to the named beneficiary on the account, regardless of what the will says.

If you have a pension, a life insurance policy, or retirement accounts — 401(k), IRA, superannuation, workplace pension — that still name a previous beneficiary, or that name no beneficiary, the marriage is the trigger to update these designations. A will that leaves everything to your spouse is ineffective with respect to pension and life insurance assets if the beneficiary designation on those accounts names someone else.

Update beneficiary designations as a separate, parallel exercise to drafting your will.

What Happens Without a Will: Intestacy Laws by Country

Understanding the intestacy default in each jurisdiction where you hold assets is the clearest illustration of why a will is necessary. These defaults may not be what you would choose.

India

Under the Hindu Succession Act, the estate of a Hindu person who dies without a will is distributed among Class I heirs — the spouse, sons, daughters, mother, and certain other specified relatives in specific circumstances. If the deceased has a surviving spouse and children, the estate is divided equally among the spouse and the children.

For a newly married NRI without children, the Hindu Succession Act directs the estate to the spouse and the mother in equal shares — meaning the spouse receives half the estate and the deceased's mother receives the other half, subject to the specific terms of the Act.

For NRI couples where the surviving spouse is the primary intended beneficiary of the entire estate, this default allocation — which does not give the full estate to the spouse — may not reflect their wishes.

Under Muslim personal law, the inheritance structure is more complex — heirs are classified in a specific order and receive fixed fractional shares defined by Islamic jurisprudence. The surviving spouse receives a defined fraction, with the remainder distributed among other heirs according to the applicable rules.

United Kingdom

In England and Wales, if a person dies intestate — without a will — the estate is distributed according to the intestacy rules under the Administration of Estates Act 1925 as amended.

For a married person dying without children: the surviving spouse inherits the entire estate. For a married person dying with children: the surviving spouse receives all personal possessions, a statutory legacy of £322,000 (as of the current rules), and half of the remainder. The children receive the other half of the remainder.

For a newly married NRI without children, the UK intestacy rules do direct the entire estate to the surviving spouse — which may align with wishes. However, the rules do not address cross-border assets, do not specify guardianship wishes, do not include specific bequests, and do not provide any of the other directions that a comprehensive will provides.

United States

US intestacy law is governed at the state level, and rules vary significantly between states. In most states, if a person dies intestate with a surviving spouse but no children, the surviving spouse inherits the entire estate. In some states, a portion passes to the deceased's parents if living.

In community property states — California, Texas, Arizona, and others — assets acquired during the marriage are community property and pass to the surviving spouse automatically. Separate property — assets acquired before the marriage or by gift or inheritance during the marriage — is distributed according to the intestacy rules.

For NRI couples in the US, the community property versus separate property distinction is particularly important for recently married couples. Assets acquired before the marriage — which for established NRI professionals may represent the majority of their accumulated wealth — are separate property and are distributed according to the potentially less favourable intestacy rules.

Canada

Canadian intestacy law is provincial. In Ontario — the province with the largest NRI community — if a person dies intestate with a surviving spouse and no children, the surviving spouse inherits the entire estate. With a surviving spouse and children, the spouse receives a preferential share — currently $350,000 — and the remainder is divided between the spouse and children according to specific proportions.

Provincial intestacy rules vary. British Columbia, Alberta, and other provinces have their own specific frameworks. The general principle — that the surviving spouse does not automatically receive the entire estate in all circumstances — applies across most provinces.

Australia

Australian intestacy law is state-governed. In most states, if a person dies intestate with a surviving spouse and no children, the entire estate passes to the surviving spouse. In New South Wales — the state with a significant NRI community — if there are both a surviving spouse and children, the spouse receives all household goods, a statutory legacy, and a share of the remainder. The children share the rest.

Superannuation does not form part of the deceased estate — it is distributed by the superannuation fund trustee based on the binding death benefit nomination or, in the absence of a binding nomination, the trustee's discretion. This is a critically important distinction for Australia-based NRI couples. Your superannuation — which may represent a significant portion of your Australian-held wealth — is not controlled by your will.

UAE

The UAE's personal status law applies personal law to succession matters — Islamic law for Muslim residents, with specific provisions for non-Muslim expatriates.

For non-Muslim expatriates in the UAE, the position on succession has evolved following legislative changes in recent years. Under updated UAE federal law, non-Muslim expatriates can now register a will in the UAE under the law of their home country, or register a will under the UAE Civil Personal Status Law for non-Muslims. Prior to these legislative changes, UAE courts would typically apply the law of the deceased's home country to their estate — which created uncertainty and complexity for NRI families navigating UAE succession.

For UAE-based NRI couples, having a registered UAE will — alongside wills in other relevant jurisdictions — is increasingly important as UAE succession law develops.

The Dubai International Financial Centre (DIFC) Wills Service offers a well-established will registration service for non-Muslim expatriates in the UAE, providing a clear legal framework for the distribution of UAE-held assets.

The Multi-Jurisdictional Will: The Central Challenge for NRI Couples

The central challenge of will planning for NRI couples is that a single will is often not sufficient. Assets in different countries are governed by different succession laws, and a will that is valid and effective in one jurisdiction may not be valid or effective in another.

The Mirror Will Approach

One common approach for NRI couples with assets in multiple jurisdictions is the mirror will approach — creating separate wills in each relevant jurisdiction, each dealing with the assets in that jurisdiction, and each drafted to be consistent with the others.

A UK will deals with UK assets — property, bank accounts, investments, pension funds held in the UK. An Indian will deals with Indian assets — property, NRE and NRO accounts, Indian investments. If there are significant assets in a third country, a third will may be needed.

The mirror wills need to be carefully coordinated — if the UK will contains a general residuary clause that purports to cover all assets not otherwise dealt with, it may inadvertently conflict with the Indian will. The wills need to be drafted with awareness of each other to prevent conflicts.

The Governing Law Clause

Wills often contain a governing law clause — a provision specifying which country's law governs the interpretation and administration of the will. This clause is important for NRI wills because it establishes the legal framework within which the will is read.

For a UK will, English law as the governing law provides a clear, well-established framework. For an Indian will, Indian law as the governing law reflects the framework under which Indian assets are administered.

The governing law clause does not override the local law of the country where specific assets are located — immovable property in India is subject to Indian succession law regardless of what a foreign will says. But it provides clarity on interpretation questions and reduces ambiguity in the administration process.

The Situs Rule for Immovable Property

The most important jurisdictional principle for multi-country estate planning is the situs rule — the rule that immovable property is governed by the law of the country where it is located, regardless of the deceased's domicile or the governing law of their will.

This means that property in India is governed by Indian succession law — specifically the applicable personal law. A UK will or US will that directs the distribution of all assets may not effectively control what happens to Indian property if the applicable Indian law has different mandatory requirements.

For NRI couples with Indian property — which is most NRI couples with family connections to India — this rule means that the Indian will is not optional. It is required if the couple wants to exercise any control over what happens to the Indian property.

Domicile: The Most Important Concept in International Estate Planning

Domicile — the concept that determines which country's succession law governs a person's personal and movable property — is the most important and most frequently misunderstood concept in international estate planning.

Domicile is not the same as residence. You can reside in the UK for many years while maintaining an Indian domicile. Domicile of origin — the domicile you are born with, based on your father's domicile at the time of your birth — persists until it is replaced by a domicile of choice. A domicile of choice is acquired by taking up residence in a country with the intention of remaining there permanently or indefinitely.

For NRI couples, the domicile question is often genuinely uncertain. A person who has been in the UK for twenty years but who has always maintained the intention of eventually returning to India may have retained their Indian domicile — which means that Indian succession law governs their movable property worldwide.

The domicile question has significant practical consequences for which country's succession law applies to movable assets — bank accounts, investments, shares — held in different countries. It needs to be assessed specifically for each NRI individual as part of the estate planning process.

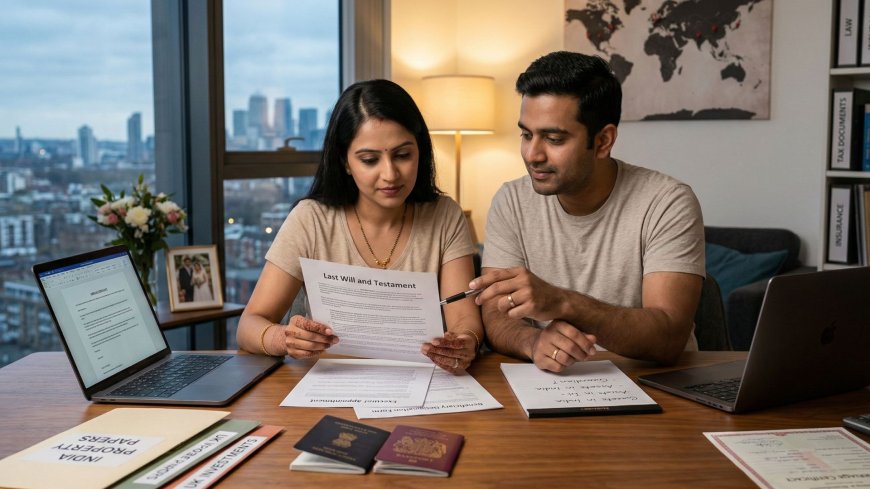

Creating a Will: Practical Steps for NRI Couples

Step One: Take Inventory of Your Assets Across All Jurisdictions

Before engaging any legal advisers, create a comprehensive inventory of your assets — organised by jurisdiction.

United Kingdom assets: property, bank accounts, ISAs, investment portfolios, pension funds, life insurance, business interests. Indian assets: property, NRE and NRO accounts, Indian investments, Indian business interests, shares in family companies. US assets if applicable: 401(k), IRA, brokerage accounts, property. Australian assets if applicable: superannuation, property, bank accounts. UAE assets if applicable: property, bank accounts, DIFC or ADGM held assets.

For each asset, note the current titling — sole ownership, joint ownership, tenancy in common — and the current beneficiary designation if applicable.

This inventory is the foundation of the estate planning conversation with your legal advisers. It enables them to assess the specific jurisdictional issues that apply to your situation and to recommend the appropriate will structure.

Step Two: Identify Your Wishes

Before the legal drafting begins, be clear about what you want.

If you die first, who do you want to receive your estate? Your spouse entirely? Your spouse and children if you have them? Specific assets to specific people? What happens to assets that are held jointly with family members in India?

If both you and your spouse die simultaneously — or if your spouse predeceases you — who do you want to receive the estate? This secondary beneficiary — the contingent beneficiary — is as important as the primary one.

If you have children, or intend to have children, who do you want to act as guardian if both parents die? This is one of the most important provisions of any will for couples who are parents or who plan to become parents.

What specific assets do you want to direct to specific people? Are there family heirlooms, specific properties, or specific financial assets that you want handled in a particular way?

These wishes — clearly articulated before the legal drafting begins — give your legal advisers the instructions they need to draft wills that reflect your actual intentions.

Step Three: Engage Legal Advisers in Each Relevant Jurisdiction

Multi-jurisdictional estate planning requires legal advisers in each relevant jurisdiction — not a single adviser who will draft a single document and hope it works everywhere.

For UK assets, a UK solicitor specialising in wills and estate planning. For Indian assets, an Indian lawyer specialising in succession law and estate planning. For US assets, a US estate planning attorney in the relevant state. For Australian assets, an Australian solicitor specialising in wills and estate planning.

These advisers need to work in coordination — each aware of the others' work and ensuring that the documents they draft are consistent with each other and do not inadvertently conflict.

Engaging advisers with specific experience in cross-border estate planning — advisers who regularly work with NRI clients or internationally mobile clients — is preferable to engaging advisers whose practice is entirely domestic. The cross-border dimension adds complexity that domestic specialists may not be equipped to navigate.

Step Four: Draft, Execute, and Register

The drafting of the will — or wills — is the legal advisers' work. Your role is to review the draft carefully, confirm that it reflects your intentions accurately, and ask questions about anything that is not clear.

Execution requirements: Wills must be executed — signed and witnessed — in accordance with the formal requirements of the jurisdiction. In the UK, a will must be signed by the testator in the presence of two witnesses who are both present at the same time and who then sign the will in the testator's presence. The witnesses must not be beneficiaries. In India, a will requires the signature of the testator and two attesting witnesses. In the US, execution requirements vary by state but typically require witnesses and in some states notarisation. In Australia, similar witness requirements apply.

Errors in execution — a will that was not properly witnessed, or where a witness was also a beneficiary — can invalidate the will entirely.

Registration: In India, a will can be registered with the Sub-Registrar under the Registration Act. Registration is not mandatory — an unregistered will is legally valid. However, registration provides a layer of security — a registered will is harder to challenge and its existence is formally documented. For NRI couples with Indian assets, registering the Indian will is strongly advisable.

In the UK, wills can be stored with the Probate Registry or with a will storage service. In the US, some states allow wills to be filed with the probate court while the testator is alive. In Australia, wills can be stored with the state Supreme Court or with a commercial will storage service.

Specific Provisions NRI Couples Should Include

The Survivorship Clause

A survivorship clause — specifying that a beneficiary must survive the testator by a defined period, typically 30 days, to inherit under the will — is particularly important for NRI couples. Without this clause, if both spouses die in the same accident — a plane crash, a road accident — and one survives the other by hours, the estate of the first to die passes to the survivor and then immediately into the survivor's estate, potentially passing to different beneficiaries than the first deceased would have chosen.

A 30-day survivorship clause prevents this — if the spouse does not survive for 30 days, the estate passes directly to the contingent beneficiary rather than through the spouse's estate.

Guardianship Provisions

If the couple has children — or plans to have children — the guardianship provision is one of the most important provisions of any will. This provision names the person or people who will have physical custody of the children if both parents die. Without a guardianship provision, the court decides who raises your children.

For NRI couples, the guardianship question is often complex — the preferred guardian may be in India, while the children are in the UK or the US. The practicalities of international guardianship — including the laws of the country where the guardian lives — need to be considered in the guardianship provision.

The Letter of Wishes

Alongside the formal will, a letter of wishes — a non-legally binding document that provides guidance to the executors and family on matters that are not appropriate for inclusion in the will itself — is a valuable companion document.

The letter of wishes might address: the deceased's wishes for funeral and cremation. Guidance on how specific assets — family heirlooms, jewellery, sentimental items — should be distributed if not specifically bequeathed in the will. Messages to family members. Guidance on how the estate should be managed during the administration period.

The letter of wishes is not legally binding but provides invaluable context and guidance for the people managing the estate.

Digital Assets

The treatment of digital assets — cryptocurrency holdings, online investment accounts, digital collectibles, subscription services, social media accounts, domain names — is an increasingly important will consideration that many estate planning documents do not yet adequately address.

For NRI couples with cryptocurrency holdings or other digital assets, the will should address these specifically — including access instructions, in a secure form, for executors who will need to access digital accounts.

Beneficiary Designations: The Documents That Work Alongside Your Will

As noted earlier, certain assets pass outside the estate entirely — they are not governed by the will but by the beneficiary designation on the account.

Assets That Pass by Beneficiary Designation

UK workplace pensions and personal pensions. UK life insurance policies. US 401(k) and IRA accounts. US life insurance policies. Australian superannuation. Canadian RRSP and RRIF accounts. Life insurance policies in any jurisdiction.

These assets require separate, consistent beneficiary designation updates. After the wedding, review every pension, retirement account, and life insurance policy you hold. Update the beneficiary designation to reflect your current wishes — typically naming your spouse as the primary beneficiary and a contingent beneficiary if the spouse predeceases you.

A will that directs your estate to your spouse is entirely ineffective with respect to your pension if the beneficiary designation on the pension names your parents or a previous partner. The beneficiary designation overrides the will for these assets.

The Superannuation Binding Death Benefit Nomination

In Australia, the superannuation binding death benefit nomination is particularly important — and particularly time-limited. A binding nomination is typically valid for three years, after which it lapses. An expired nomination means the trustee has discretion over how the superannuation is distributed.

After the wedding, update your Australian superannuation binding death benefit nomination to name your spouse. And set a reminder to renew it before the three-year expiry.

Reviewing and Updating Your Will

A will is not a permanent, unchanging document. It needs to be reviewed and updated as circumstances change.

Events that should trigger a will review: the birth of a child. A significant change in assets — acquiring or selling property, significant increase or decrease in wealth. A change in your country of residence. A change in the family situation of a named beneficiary or guardian. A change in family relationships — estrangement, bereavement. A significant change in tax law that affects the estate planning structure.

For NRI couples who may relocate multiple times during their careers, each relocation to a new country is a trigger for a will review — the new country's succession laws need to be addressed, and the existing wills need to be assessed for compatibility with the new jurisdiction.

Common Mistakes Newly Married NRI Couples Make With Wills

Not Creating a Will at All

The most common and most consequential mistake. The absence of a will leaves the estate to be distributed according to intestacy rules that may not reflect the deceased's wishes, creates significant administrative complexity for the surviving spouse, and may produce outcomes — partial distribution to in-laws, division of property among multiple heirs — that cause lasting family difficulties.

Creating a Single Domestic Will and Assuming It Covers Everything

A UK will that covers UK assets does not control what happens to Indian property. An Indian will does not control Australian superannuation. Creating a single will for one jurisdiction and assuming it handles the full picture is a structurally inadequate approach for any NRI couple with multi-jurisdictional assets.

Not Updating Beneficiary Designations

A comprehensive will is rendered partially ineffective if the beneficiary designations on pensions, retirement accounts, and life insurance policies are not updated consistently. Review and update all beneficiary designations as a separate exercise from — but concurrent with — the will drafting process.

Allowing Wills to Become Outdated

A will drafted before the first child was born that does not include guardianship provisions. A will drafted in the UK before a relocation to Canada that does not address Canadian assets. A will with a beneficiary who has since died. Outdated wills create exactly the kind of confusion and inadequate distribution that the will was intended to prevent.

Not Telling Anyone Where the Will Is

A will that exists but cannot be found when it is needed is nearly as ineffective as a will that does not exist. Tell your spouse, your executor, and a trusted family member where your will is stored. If it is registered in India or stored with a UK law firm or Australian court, ensure the relevant people know how to access it.

The Most Loving Thing You Can Do After the Wedding

The will is not a morbid document. It is not an acknowledgement of doubt or a preparation for failure. It is an act of care — for your spouse, for your family, for everyone who loves you and who would be left to navigate the aftermath of your death.

It says: I have thought about this. I have made my wishes clear. I have done what I can to make the impossible easier for the people I love.

For newly married NRI couples whose lives span countries, whose assets reflect years of international effort, and whose families are bound together across generations and cultures — the will is not optional. It is the document that ensures that everything you have built together goes where you would want it to go, is managed the way you would want it to be managed, and serves the people you would want it to serve.

Create it now. Not because anything is going to happen. Because it is the right thing to do for the people who matter most to you.

The wedding celebrated the beginning. The will protects everything that follows.

Give it the attention it deserves.

What's Your Reaction?

Like

0

Like

0

Dislike

0

Dislike

0

Love

0

Love

0

Funny

0

Funny

0

Angry

0

Angry

0

Sad

0

Sad

0

Wow

0

Wow

0